TL;DR:

- Regulators worldwide clarify that tokenized assets remain subject to existing financial laws and classifications.

- Compliance involves proper token classification, licensing, KYC/AML, and careful jurisdiction selection from the start.

- Legal strategy and architecture are critical; proactive legal design prevents costly regulatory issues.

Tokenized assets do not exist in a legal vacuum. Across the United States, European Union, Singapore, and the UAE, regulators have made clear that placing an asset on a blockchain does not remove it from the scope of financial law. Tokenized assets are generally classified as securities under existing frameworks in most major jurisdictions, triggering licensing obligations, investor protection rules, and AML/CFT requirements. For crypto founders and virtual asset service providers (VASPs), this reality demands careful legal planning before a single token is minted. This guide clarifies how tokenization laws operate across key jurisdictions, compares regulatory approaches, and sets out the compliance steps your project cannot afford to skip.

Key Takeaways

| Point | Details |

|---|---|

| Global laws differ | Tokenization regulations vary across countries and shape how projects launch and operate. |

| Securities classification is common | Most jurisdictions treat tokenized assets as securities, triggering strict compliance obligations. |

| Compliance is not optional | Licensing, KYC/AML, and proper structuring are essential to avoid legal risks and penalties. |

| Legal strategy is crucial | Aligning technology and legal frameworks from the start is the key to sustainable tokenization. |

What is tokenization law and why does it matter?

Tokenization is the process of representing ownership rights in a real-world or digital asset as a token on a distributed ledger technology (DLT) network. DLT is the underlying infrastructure, of which blockchain is the most widely recognised form. The tokens produced can broadly be divided into two categories: security tokens, which represent an investment interest (such as equity, debt, or revenue share) and are subject to securities regulation; and utility tokens, which grant access to a product or service and may escape securities classification in certain jurisdictions, though not always.

Tokenization laws exist for three primary reasons:

- Investor protection: Ensuring buyers receive accurate disclosures and can seek legal recourse if things go wrong.

- Market integrity: Preventing manipulation, fraud, and systemic risk in capital markets.

- Anti-money laundering (AML) and counter-terrorism financing (CTF): Blocking illicit funds from moving through token issuances.

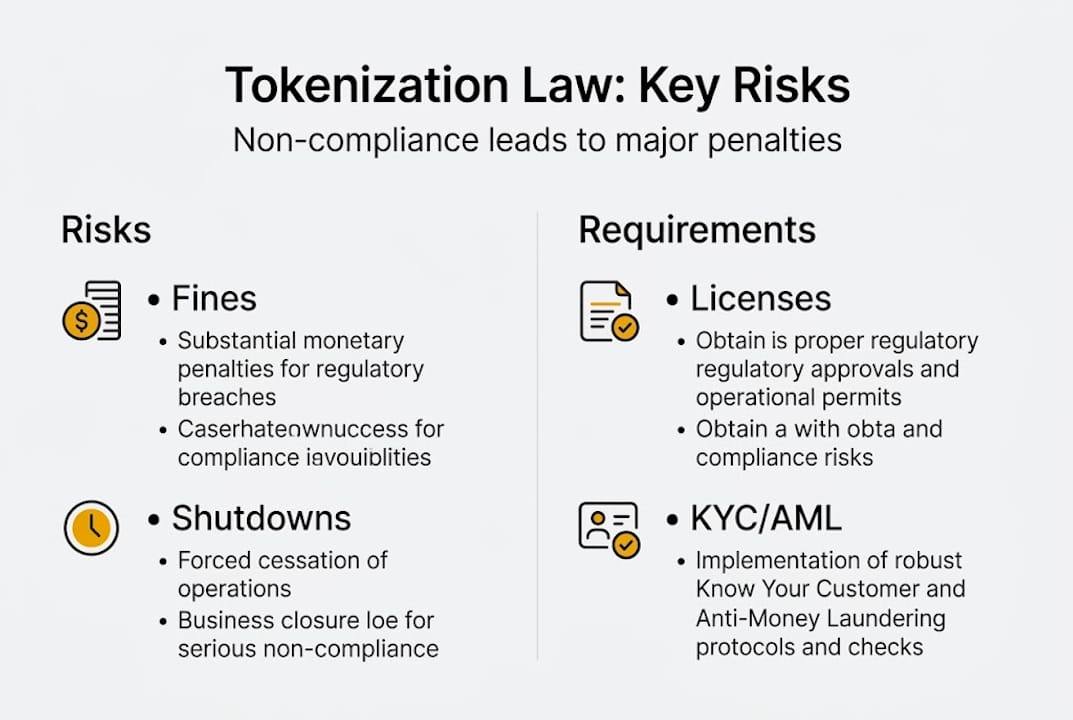

The consequences of non-compliance are severe. Regulators can impose substantial fines, order project shutdowns, and place founders on blacklists that bar them from future financial services activity. In the US, the SEC has pursued enforcement actions resulting in nine-figure penalties. In the UAE, VARA can suspend or revoke licences and refer matters to criminal prosecutors.

Legal classification also directly shapes your fundraising options. A token classified as a security in the US must comply with registration or exemption requirements before it can be offered to investors. Misclassifying a security token as a utility token is not a technical oversight; it is a regulatory violation. Tokenized assets require compliance with securities regulations, licensing, KYC/AML, and investor accreditation rules wherever they are offered.

Pro Tip: Before selecting a jurisdiction, map your token's economic rights against the legal tests applied locally. The Howey Test in the US, the MAS capital markets product definition in Singapore, and VARA's token classification matrix in Dubai each use different criteria. Getting this classification right at inception saves significant legal cost later.

For projects needing structured legal guidance from the outset, reviewing the available legal services for tokenization provides a practical starting point.

Key global jurisdictions: How tokenization laws vary

With the basics defined, here is how major jurisdictions shape tokenization law in practical terms.

| Jurisdiction | Classification approach | Key licensing requirement | Investor access | Standout feature |

|---|---|---|---|---|

| United States | Howey Test (SEC) | Broker-dealer or ATS licence for secondary trading | Reg D 506(c) accredited; Reg A+ up to $75M; Reg S offshore | Most litigated framework globally |

| Switzerland | DLT Act; FINMA guidance | Banking or securities firm licence | Professional investor exemptions | DLT ledger-based securities legally recognised |

| Singapore | Capital Markets Products (MAS) | Capital Markets Services (CMS) licence | Accredited investor exemptions | Regulatory sandbox available |

| UAE (Dubai/ADGM) | VARA/SCA/FSRA classification | FSP or VARA licence | Qualified investor thresholds | On-chain enforceability; tax-free environment |

The US framework remains the most litigated globally. The SEC applies the Howey Test to determine whether a token is a security, with exemptions available under Reg D 506(c) for accredited investors, Reg S for offshore offerings, and Reg A+ for issuances up to $75 million. Secondary trading of security tokens requires a registered broker-dealer or alternative trading system (ATS) licence.

Singapore's MAS treats tokenized assets as Capital Markets Products, requiring a CMS licence for dealing or advising. Accredited investor exemptions reduce the disclosure burden for private placements, and MAS operates a regulatory sandbox that allows innovative projects to test within defined parameters before full authorisation.

The UAE stands out for its on-chain enforceability provisions, particularly under SCA's tokenisation framework, which allows smart contract terms to carry legal weight. This is a significant advantage for real-world asset (RWA) tokenization projects. IOSCO's insights on tokenization adoption confirm that regulatory clarity, rather than technology alone, is the primary driver of institutional participation in tokenized markets.

For projects considering the UAE, understanding the distinction between digital securities versus virtual assets in UAE is essential, as is reviewing VARA token issuance rules in Dubai before structuring your offering. Broader blockchain legal requirements also apply across all jurisdictions.

Compliance requirements for crypto startups and VASPs

Knowing where laws differ, here is what compliance looks like for real-world crypto ventures.

- Classify your token correctly. Engage legal counsel to apply the relevant legal test in each target jurisdiction before any public communication about the project.

- Obtain the required licence. Depending on jurisdiction and token type, this may be a VASP registration, securities dealer licence, CMS licence, or VARA Financial Services Permission (FSP).

- Implement KYC/AML onboarding. All investors must be verified against sanctions lists and assessed for AML risk before receiving tokens. This applies regardless of whether the offering is public or private.

- Structure via a Special Purpose Vehicle (SPV). An SPV ring-fences the tokenized asset from the issuer's broader balance sheet, protecting investors in the event of issuer insolvency.

- Vet investors against eligibility criteria. Confirm accredited, professional, or qualified investor status where required by the applicable exemption.

- Geofence your offering. Restrict access to investors in jurisdictions where you hold no licence or valid exemption. This is typically implemented at the platform and smart contract level.

- File ongoing regulatory reports. Most jurisdictions require periodic reporting on token supply, investor numbers, and AML activity.

Crypto startups and VASPs must structure via SPV, geofence offerings, and prioritise KYC/AML integration in smart contracts, particularly using the ERC-3643 standard, which enables on-chain identity verification and transfer restrictions. Jurisdiction selection should align with the geographic profile of your investor base.

Public chain issuance carries higher regulatory exposure than permissioned networks. On a public blockchain, any wallet can receive tokens unless transfer restrictions are coded into the contract. The SCA's on-chain framework addresses this by requiring whitelisting mechanisms that restrict transfers to verified wallets only.

Pro Tip: Integrate compliance controls at the smart contract layer from day one. Retrofitting KYC/AML logic into a deployed contract is technically complex and legally risky. Standards such as ERC-3643 allow you to embed transfer restrictions, investor eligibility checks, and forced transfer capabilities directly into the token architecture.

For a structured approach to token legal design, the token legal frameworks for Web3 resource outlines the key considerations, while KYC/AML for tokenized projects covers AML policy requirements in detail.

Edge cases and legal innovations in tokenization

Compliance is rarely straightforward; the reality is shaped by exceptions and cutting-edge legal tactics.

| Scenario | Permissioned DLT | Permissionless DLT |

|---|---|---|

| Issuer liability | Lower; controlled participant set | Higher; open transfer risk |

| Licence requirement | Often reduced | Full licensing typically required |

| OTC trading limits | Negotiable with regulator | Standard restrictions apply |

| Insolvency framework | SPV ring-fencing effective | Requires additional legal safeguards |

Edge cases in tokenization include the distinction between permissioned and permissionless DLT, OTC trading restrictions, wallet whitelisting obligations, and insolvency protection via SPV ring-fencing. Each of these scenarios requires specific legal treatment.

New legal and technical tools are emerging to address these complexities:

- Oracle and legal bridges: Smart contracts can be linked to off-chain legal agreements via oracle services, ensuring that on-chain token transfers carry enforceable legal effect in the relevant jurisdiction.

- Wallet whitelisting: Restricting token transfers to pre-approved, KYC-verified wallets reduces regulatory exposure on public chains.

- Third-party custodians: Appointing a regulated custodian to hold underlying assets provides an additional layer of investor protection and satisfies custody requirements in jurisdictions such as the UAE and Singapore.

- SPV ring-fencing: Structuring the tokenized asset within an SPV ensures that in the event of issuer insolvency, investor claims attach to the SPV's assets rather than the issuer's general estate.

Looking ahead, the industry is moving towards interoperability between tokenization platforms, T+1 settlement for tokenized securities, and standardised custody and oracle frameworks. Regulators including MAS and VARA are actively consulting on these developments. For projects already considering the insolvency dimension, the analysis of issuer insolvency in tokenization provides jurisdiction-specific guidance on how ring-fencing is treated under VARA's framework.

The reality most guides miss: Why legal strategy matters more than the code

Most tokenization guides focus heavily on the technology stack and lightly on legal architecture. This is the wrong emphasis. In our advisory work across VARA, SCA, FSRA, and international jurisdictions, the projects that fail at scale almost always share a common pattern: the legal structure was treated as an afterthought, addressed only when a regulator asked a question the founders could not answer.

The uncomfortable truth is that a technically flawless smart contract built on a legally deficient structure will not survive regulatory scrutiny. Proactive dialogue with regulators, robust investor documentation, and a jurisdiction selection strategy grounded in your actual investor base consistently matter more than perfect code.

Successful tokenization projects integrate legal clarity from the first day of design. The token classification, SPV structure, and compliance controls are not bolt-on features; they are foundational architecture. Founders who seek legal support for token launches early in the process consistently reach market faster and with fewer enforcement risks than those who retrofit compliance after launch.

Get expert legal guidance for your tokenization project

Legal clarity is not a constraint on tokenization; it is the foundation that makes compliant, scalable issuance possible. Whether you are structuring a real-world asset offering under VARA, navigating SCA's on-chain framework, or preparing a cross-border issuance across multiple jurisdictions, the right legal advice at the right stage prevents costly regulatory setbacks.

CRYPTOVERSE Legal Consultancy advises crypto startups and established VASPs on the full spectrum of tokenization legal experts services, from token classification and SPV structuring to licence applications and AML policy design. Our team holds deep experience with VARA licensing guidance and cross-border issuance frameworks. For a structured approach to your project, our tokenization structuring advice service covers every stage from pre-application to post-issuance compliance. Schedule a consultation to assess your project's regulatory position before you build.

Frequently asked questions

Are all tokenized assets considered securities?

In most major jurisdictions, tokenized assets are classified as securities and must comply with applicable securities regulations, including registration, disclosure, and investor eligibility requirements. Utility tokens may be exempt in certain circumstances, but this depends on the specific legal test applied locally.

What licences do I need to issue tokenized assets in the UAE?

Depending on your asset class and structure, you will likely require a VARA or SCA licence in Dubai or the broader UAE. ADGM and FSRA licences apply within the Abu Dhabi Global Market free zone. Always obtain jurisdiction-specific legal advice before proceeding.

How do KYC/AML requirements apply to on-chain assets?

KYC and AML checks can be embedded directly into smart contracts using standards such as ERC-3643, enabling on-chain identity verification and automated transfer restrictions to whitelisted wallets that meet investor eligibility criteria.

What are the risks of issuing tokens on public blockchains?

On public blockchains, issuer liability is higher because any wallet can receive tokens unless transfer restrictions are embedded in the contract. Additional controls such as whitelisting and SPV ring-fencing are required to manage regulatory exposure and protect investors.

Can retail investors buy tokenized assets?

Eligibility varies by jurisdiction. In the US, Reg D 506(c) restricts access to accredited investors, while Reg A+ allows broader retail participation up to $75 million. Switzerland and Singapore apply professional investor exemptions for most private placements, though retail-accessible structures exist within defined regulatory limits.