TL;DR:

- Real estate tokenisation in Dubai allows fractional ownership with low investment thresholds, attracting new investors.

- The process involves strict regulatory approval, legal structuring, and technology development, taking several months.

- Success depends on high-quality assets, proper compliance, and realistic expectations about liquidity and timeline.

The DLD tokenisation pilot raised AED 18.5M from 224 investors, 70% of whom were first-time Dubai property buyers. That single data point signals a structural shift rather than a passing trend. Real estate tokenisation is enabling developers to reach genuinely new pools of capital, while investors who previously lacked the ticket size to enter Dubai's property market now hold fractional ownership with real economic rights. This guide covers every material step: what tokenisation involves, the legal and regulatory prerequisites, the practical process from asset selection to token issuance, and the risks you must account for before committing capital or development resources.

Key Takeaways

| Point | Details |

|---|---|

| Fractional investment access | Tokenisation lets you invest in premium UAE real estate from AED 2,000 upwards. |

| Regulation-driven growth | Dubai's regulatory progress makes tokenisation safer and drives rapid adoption among new investors. |

| Not a 'quick flip' | Expect lower secondary liquidity than REITs and avoid tokenisation for short-term capital needs. |

| Preparation is crucial | Success requires robust legal compliance, stakeholder alignment, and realistic cost assessment. |

What is real estate tokenisation and why is it gaining ground in the UAE?

Real estate tokenisation is the process of converting ownership rights in a physical property into digital tokens recorded on a blockchain. Each token represents a proportional share of the underlying asset, including rights to rental income and capital appreciation. Crucially, these tokens are legally backed instruments, not speculative digital assets. The regulated RWA (real world asset) structure ensures that token holders have enforceable claims against the property, distinguishing tokenised real estate from crypto speculation entirely.

The UAE has become the dominant global market for this asset class. UAE tokenised real estate accounts for $3.2B, representing 42% of global volume. That concentration is not accidental. It reflects deliberate regulatory design, a mature property market with high-value assets, and a sophisticated investor base drawn from across the globe.

Why fractional ownership is changing the investment landscape

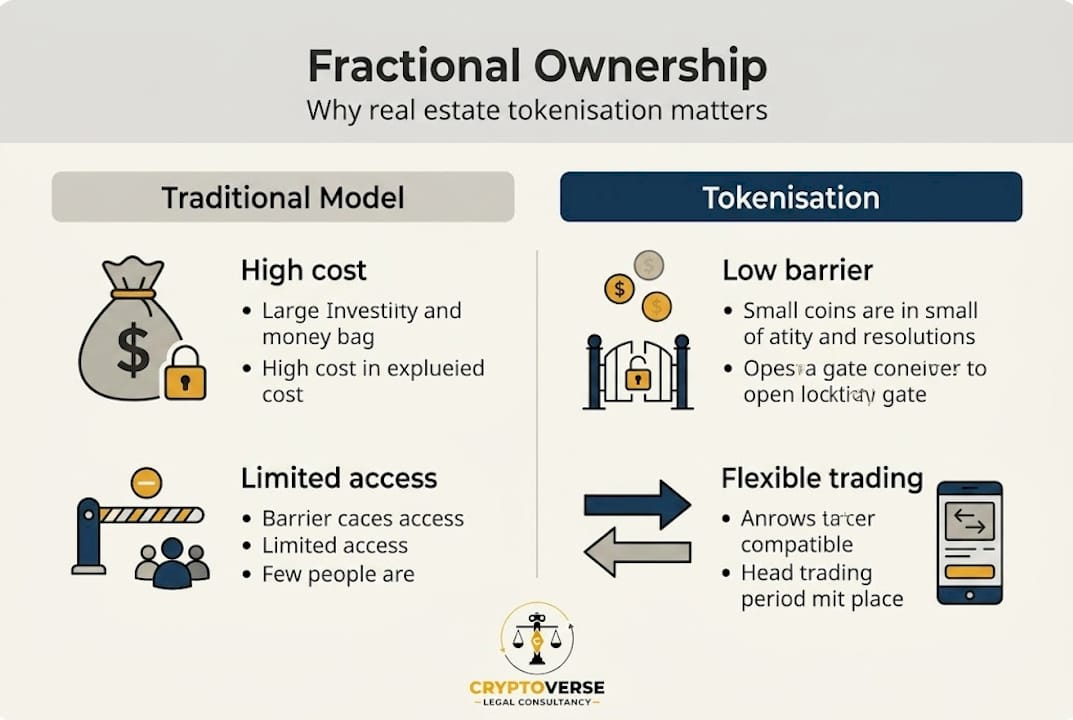

The minimum investment threshold in some tokenised Dubai offerings starts at AED 2,000. For context, the traditional minimum to participate meaningfully in Dubai residential real estate is several hundred thousand dirhams at minimum, excluding financing. Tokenisation lowers the barrier so significantly that it has attracted first-time buyers who could not previously participate at all. This is not a marginal improvement; it is a structural change to who can access this market.

Key reasons for investor uptake in the UAE include:

- Low entry thresholds enabling broad participation without large capital requirements

- Transparent yield distribution through smart contracts, reducing reliance on intermediaries

- Global accessibility allowing investors across 35+ nationalities to access Dubai property in a single offering

- Regulated legal structure providing enforceability of ownership rights under UAE law

- Secondary trading potential enabling exit routes beyond the traditional property sale cycle

| Metric | Traditional property investment | Tokenised real estate |

|---|---|---|

| Minimum investment | AED 500,000+ | From AED 2,000 |

| Investor base | Domestic/regional HNWIs | Global retail and institutional |

| Settlement period | Weeks to months | Near-instant on secondary markets |

| Regulatory oversight | DLD | DLD + VARA |

| Exit mechanism | Open market sale | Secondary token trading |

The Dubai real estate tokenisation programme represents a world-first in regulatory scope, combining the Dubai Land Department's property registry with VARA's virtual asset oversight. This dual-regulator structure gives both developers and investors a level of legal certainty that other jurisdictions have not yet achieved at scale.

Preparing for tokenisation: prerequisites, legal frameworks, and key stakeholders

Before you can issue a single token, a significant amount of legal, structural, and operational groundwork is required. Attempting to shortcut this phase is the primary reason tokenisation projects fail or attract regulatory scrutiny.

What assets qualify for tokenisation in the UAE?

The DLD pilot established secondary trading go-live dates and confirmed that high-value residential and commercial properties are eligible. Practically speaking, the asset must have clear title, be free of material encumbrances, and carry sufficient valuation to justify the costs of tokenisation infrastructure. Projects below approximately AED 3.7M in asset value often find that fixed costs erode returns to an unacceptable degree.

Regulatory prerequisites

The UAE's tokenisation framework sits across multiple regulators depending on jurisdiction and activity type. The principal bodies you need to engage are:

- Dubai Land Department (DLD): Registers tokenised property rights and oversees the real estate component

- Virtual Assets Regulatory Authority (VARA): Licenses and supervises token issuance and secondary trading within Dubai (excluding DIFC)

- Dubai Financial Services Authority (DFSA): Relevant for tokenisation activities conducted within DIFC

- Securities and Commodities Authority (SCA): Has jurisdiction over tokenised securities at the federal level

Understanding UAE crypto regulations in their full detail is essential before selecting your operating jurisdiction. The choice between onshore Dubai, DIFC, and ADGM carries material consequences for licensing requirements, investor eligibility, and token classification.

Compliance requirements you must address before launch

- Corporate entity formation and structure, including beneficial ownership documentation

- AML/CFT policy aligned with FATF standards and UAE Federal AML Law No. 20 of 2018

- KYC procedures for all token purchasers, including ongoing monitoring obligations

- VARA licence application or DFSA authorisation, depending on jurisdiction

- Smart contract audit by an accredited third-party provider

- Investor disclosure documentation, including risk warnings and yield projections

- DLD registration of the tokenised title

Key stakeholders in a tokenisation project

Every successful tokenisation involves a defined set of parties with clearly delineated responsibilities:

- Property developer or asset owner: Provides the underlying asset and economic rights

- Token issuer: The regulated entity responsible for structuring and issuing the tokens

- Legal counsel: Ensures structural compliance, drafts offering documents, and advises on regulatory classification

- Technology provider: Builds or configures the tokenisation platform, including smart contracts

- Compliance officer: Oversees AML/KYC implementation and ongoing regulatory reporting

- Auditor: Independently verifies financials, smart contracts, and asset valuations

For navigating the legal process specifically, legal counsel with direct VARA and DLD experience is not optional. Regulatory feedback cycles can be shortened materially with the right advisory support.

Pro Tip: Prepare a full documentation pack before initiating any regulator engagement. This includes title deeds, corporate structure charts, draft AML policies, smart contract specifications, and investor disclosure documents. Regulators move faster when submissions are complete on first presentation.

Step-by-step guide: how to tokenise real estate in the UAE

With your legal and regulatory prerequisites addressed, the tokenisation process itself follows a defined sequence. Each step carries specific requirements, responsible parties, and realistic timeframes.

-

Asset selection and legal due diligence Confirm the property's title status, valuation, encumbrances, and rental yield history. Commission an independent valuation. Legal counsel reviews title for tokenisation suitability. Typical timeframe: two to four weeks.

-

Structuring the tokenisation vehicle Establish the Special Purpose Vehicle (SPV) or equivalent legal entity that will hold the property and issue tokens. Determine token classification under VARA rules, whether as a utility token, security token, or real estate investment token. Review VARA token issuance rules to confirm the correct category. Typical timeframe: three to six weeks.

-

Regulatory licence application Submit VARA licence application or DFSA authorisation request with full supporting documentation. Under VARA Category 1 ARVA classification, issuers of real estate tokens must meet specific capital adequacy, governance, and operational requirements. Typical timeframe: eight to sixteen weeks, subject to regulator workload.

-

Platform selection and smart contract development Select a tokenisation platform with secondary trading functionality, robust custody arrangements, and a track record of DLD compliance. Commission smart contract development and schedule a third-party audit. Do not proceed to issuance without a clean audit report.

-

DLD registration Tokenised ownership rights must be registered with the Dubai Land Department. This step formalises the legal nexus between the on-chain token and the off-chain property title. Liaise with DLD's tokenisation team directly and submit all required documentation simultaneously with platform readiness.

-

Token issuance and investor onboarding Launch the token offering with full KYC/AML processes activated. Issue tokens to verified investors and distribute ownership confirmations. Confirm smart contract execution against the offering terms.

-

Secondary market activation Phase 2 of the DLD pilot saw secondary trading go live in February 2026, with the second offering selling out in under two minutes from 149 investors across 35 nationalities. Building secondary market access into your platform from day one is critical to investor confidence.

| Step | Responsible party | Typical timeframe |

|---|---|---|

| Asset due diligence | Developer + legal counsel | 2 to 4 weeks |

| SPV structuring | Legal counsel + corporate adviser | 3 to 6 weeks |

| VARA licence application | Legal counsel + compliance officer | 8 to 16 weeks |

| Platform and smart contract | Technology provider + auditor | 6 to 10 weeks |

| DLD registration | Legal counsel + DLD | 2 to 4 weeks |

| Token issuance | Token issuer + platform | 1 to 2 weeks |

| Secondary market launch | Platform + exchange | Ongoing post-issuance |

Pro Tip: Select platforms with robust, proven secondary trading functionality before any other technical decision. A token that cannot be traded after issuance carries significant investor relations and reputational risk, particularly in a market where liquidity expectations are high. Review the tokenisation cost breakdown carefully at structuring stage to model viability before committing.

Risks, challenges, and how to avoid common pitfalls

Understanding the operational steps is necessary but not sufficient. The most consequential decisions in tokenisation relate to risk identification and mitigation, not execution mechanics.

Principal risks

-

High fixed costs eroding small raises: Regulatory, legal, technology, and audit costs in a UAE tokenisation project are broadly fixed regardless of raise size. For raises below AED 3.7M, these costs routinely erode project economics to an unviable level.

-

Secondary market illiquidity: Secondary market turnover for tokenised property sits at approximately 0.02% to 0.15%, compared to 1% to 3% for REITs. Developers and investors who assume they can exit quickly through secondary markets should treat this as a material constraint, not a footnote.

-

Cross-border regulatory uncertainty: Token sales to investors in jurisdictions outside the UAE introduce additional compliance obligations. US, EU, and certain Asian markets each impose their own requirements on token offerings, and failure to address these at issuance can create post-launch legal exposure.

-

Smart contract vulnerabilities: A single unaudited or inadequately tested smart contract can result in asset loss, investor disputes, or regulatory sanctions. This is not a theoretical risk; it has occurred in tokenisation projects globally.

-

Platform counterparty risk: Choosing an unregulated or under-capitalised platform introduces custodial and operational risks that no amount of structural elegance can offset.

Common misconceptions that lead to failure

A recurring pattern in failed tokenisation projects involves promoters who believe tokenisation is a cheap and fast capital route, particularly for raises under AED 3.7M (approximately $1M). It is neither. The compliance burden, platform costs, and regulatory timelines make tokenisation a tool for well-capitalised, quality projects, not a shortcut for developers who cannot access conventional financing.

"Real estate tokenisation is not a tool for raising capital you need in less than three months. The regulatory timeline, smart contract development cycle, and investor onboarding process alone typically span six months minimum."

How to mitigate the principal risks

- Stress-test your business model at three different raise scenarios: expected, conservative, and worst case

- Use only VARA-regulated or DFSA-authorised platforms with independently audited smart contracts

- Engage legal counsel with direct experience of cross-border token offering compliance, not just UAE domestic law

- Build secondary market functionality into platform requirements before signing any technology contract

- Review regional tokenisation differences across GCC markets if your investor base extends beyond the UAE, as regulatory expectations diverge significantly

- Understand that tokenising luxury real estate in high-value segments tends to produce the strongest risk-adjusted economics given fixed cost absorption

The reality behind the tokenisation hype: what experienced practitioners have learned

Having observed multiple tokenisation projects from pre-structuring through to post-issuance, a clear pattern emerges. Projects that succeed consistently share the same characteristics: they involve high-quality assets, well-capitalised developers, thorough regulatory preparation, and realistic investor expectations. Projects that struggle almost always entered the process believing tokenisation would shortcut the hard work of capital raising.

The best outcomes in tokenisation occur when it is used to broaden access to a deal that is already well-structured and commercially sound. Tokenisation amplifies quality. It does not create it. First-mover projects in the UAE, particularly the DLD pilots, succeeded precisely because they were underpinned by credible assets, a rigorous regulatory framework, and platforms capable of delivering investor-grade execution.

The lesson for developers and investors considering tokenisation in 2026 is straightforward. Approach VARA-compliant tokenisation as you would any regulated securities offering: with adequate capital, professional advisers who know the specific regulatory pathway, and a realistic timeline measured in months, not weeks. The market rewards preparation and penalises shortcuts with regulatory delays, investor disputes, and reputational damage that is difficult to reverse.

Expert support for your real estate tokenisation journey

Navigating VARA licensing, DLD registration, AML/CTF compliance, and smart contract governance simultaneously requires a legal team that understands both the regulatory framework and the technology stack in equal measure.

CRYPTOVERSE Legal Consultancy provides end-to-end support for real estate tokenisation projects in the UAE, from initial asset structuring and regulatory classification through to VARA licence submission and post-issuance compliance. Our tokenisation legal experts have direct experience advising across VARA, DFSA, FSRA, and SCA frameworks. For developers and investors ready to move from concept to compliant token issuance, our real estate tokenisation consultancy provides a structured pathway that reduces timeline risk and maximises regulatory certainty from day one.

Frequently asked questions

What assets can be tokenised in the UAE?

Most commercial and residential real estate can be tokenised, provided the asset meets full regulatory compliance and documentation requirements. The DLD pilot phases have already tokenised high-value luxury properties, establishing a clear precedent for asset eligibility.

How liquid are tokenised real estate assets compared to REITs?

Secondary market turnover for property tokens sits at 0.02% to 0.15%, substantially below the 1% to 3% typical for REITs, making tokenised real estate better suited to investors with medium to long-term horizons.

What is the minimum investment for property tokens in the UAE?

Minimum investment in some tokenised Dubai properties starts at AED 2,000, enabling fractional access for a broad range of investors who could not previously participate in direct property ownership.

Is tokenisation suitable for short-term capital needs?

No. Tokenisation is not suitable for investors or developers requiring liquidity in under three months, given the regulatory timelines, platform onboarding requirements, and secondary market constraints inherent to the asset class.