TL;DR:

- The UAE's complex multi-regulator environment requires precise activity mapping and token classification for crypto licensing. Regulatory regimes differ across zones and activities, demanding tailored compliance strategies for each virtual asset service provider. Accurate activity and asset mapping are critical to ensure successful licensing and ongoing regulatory adherence in the UAE.

The UAE has positioned itself as one of the world's most active digital asset jurisdictions, yet the regulatory architecture governing virtual asset service providers is considerably more layered than most founders and compliance teams anticipate. Five distinct regulators operate across federal and free zone jurisdictions, each with its own statutory remit, licensing categories, and technical requirements. The introduction of the Capital Market Authority's activities-based framework in 2026 has added fresh obligations alongside existing VARA, FSRA, and CBUAE regimes. This article maps the full landscape and provides actionable guidance on licensing, activity mapping, and compliance for crypto startups and established VASPs operating in or entering the UAE.

Key Takeaways

| Point | Details |

|---|---|

| Regulatory scope clarity | UAE crypto regulation is multi-layered, with federal, free zone, and payment token authorities each setting unique requirements. |

| Activities-based licensing | CMA mandates licensing categories for eight specific virtual asset activities, requiring tailored compliance per activity. |

| Token classification matters | Each token must be risk-assessed and matched to regulator categories, which drives licensing and compliance obligations. |

| Evidence-based onboarding | Regulators expect repeatable, risk-based evidence packs, not one-off reviews, especially for ADGM-authorised activities. |

| Avoid mapping pitfalls | Accurately linking your business activities and asset mechanics to the right regulatory categories prevents costly licensing delays. |

Understanding the UAE crypto regulatory landscape

The UAE does not operate under a single unified crypto regulator. Instead, authority is distributed across multiple bodies depending on the type of virtual asset activity, the geographic zone in which a business operates, and the nature of the tokens involved. Understanding this distribution is the essential first step before any licensing application.

The four primary regulators you need to know are:

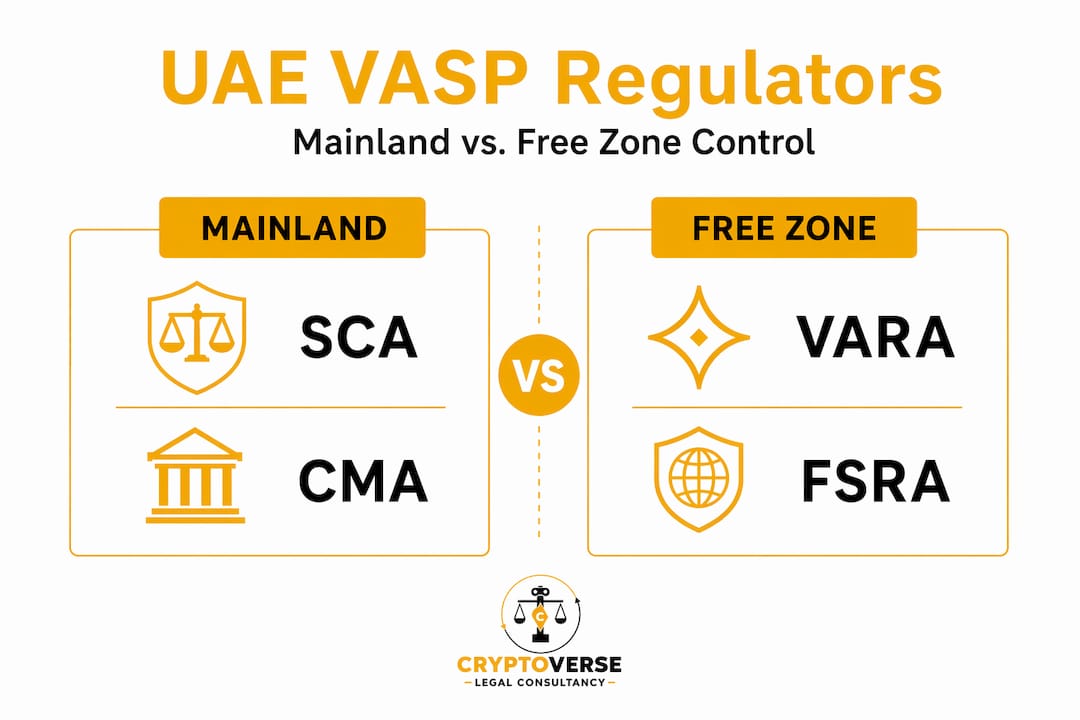

- Securities and Commodities Authority (SCA) / Capital Market Authority (CMA): The primary federal authority for virtual assets across the UAE mainland. MoF guidance designates SCA as the lead federal regulator, explicitly excluding financial free zones and payment token services from its remit.

- Central Bank of the UAE (CBUAE): Regulates payment token services, including stablecoins and digital payment instruments, at the federal level.

- Virtual Assets Regulatory Authority (VARA): Governs virtual asset activities within the Emirate of Dubai, outside the Dubai International Financial Centre (DIFC).

- Financial Services Regulatory Authority (FSRA) of ADGM: Regulates virtual asset activities within the Abu Dhabi Global Market financial free zone.

The distinction between mainland and financial free zone regulation is a persistent source of confusion. The DIFC operates under the Dubai Financial Services Authority (DFSA), while ADGM operates under the FSRA. Both are financially autonomous zones with their own rulebooks. A business licensed by VARA cannot automatically conduct regulated activities within DIFC or ADGM, and vice versa. For a thorough overview of how these regimes interact, the UAE crypto compliance overview provides useful foundational context.

Regulatory allocation also depends on the specific activity being conducted. Dealing in investment tokens on the mainland falls under SCA/CMA jurisdiction. Issuing or exchanging payment tokens triggers CBUAE oversight. Operating an exchange or providing custody in Dubai (outside DIFC) requires VARA authorisation. This activity-by-zone matrix means that many businesses will need to engage more than one regulator, particularly those with diversified product offerings. For businesses building Web3 infrastructure or multi-product platforms, the web3 compliance in the UAE guide outlines how these layers interact in practice.

The new federal VASP framework: activities-based licensing

The CMA issued a new federal VASP framework in 2026, consolidating virtual asset licensing into an activities-based model. Rather than issuing a single broad licence, the framework requires applicants to identify and apply for authorisation in respect of each specific regulated activity they intend to conduct.

The eight regulated virtual asset activities under the CMA framework are:

- Dealing as principal in virtual assets

- Dealing as agent on behalf of clients

- Providing custody of virtual assets

- Arranging custody of virtual assets

- Operating a multilateral trading facility (MTF) for virtual assets

- Providing investment advice in relation to virtual assets

- Managing a portfolio of virtual assets

- Arranging investment deals in virtual assets

Each activity carries its own minimum capital requirement, governance obligations, and risk-based assessment criteria. The framework also introduces explicit cybersecurity standards and systems resilience requirements, reflecting the operational risk profile of digital asset businesses. Governance requirements include board-level accountability for compliance, documented risk management frameworks, and adequate senior management oversight.

One critical point that many applicants overlook: holding client assets is not automatically included within a custody licence. The CMA framework requires a separate prior endorsement for client asset custody, with additional obligations around segregation, reconciliation, and client money protection. This is a gating condition, meaning you cannot hold client assets without first obtaining this endorsement, regardless of your other licensed activities.

| Activity | Mainland regulator | Free zone (Dubai) | Free zone (Abu Dhabi) |

|---|---|---|---|

| Exchange / dealing | CMA | VARA | FSRA |

| Custody | CMA (+ endorsement) | VARA | FSRA |

| Investment advice | CMA | VARA | FSRA |

| Payment tokens | CBUAE | VARA | FSRA |

| Portfolio management | CMA | VARA | FSRA |

For a detailed breakdown of SCA-regulated activities and how they map to specific product types, that resource provides granular category-by-category analysis.

Pro Tip: Do not assume that operating in a free zone exempts you from all federal obligations. Payment token activities and AML/CFT obligations under federal law apply regardless of zone. Always assess both the zone-specific and federal regulatory layers before structuring your entity.

ADGM and FSRA: token-scoping and activity authorisation

Within the Abu Dhabi Global Market, the FSRA applies a distinct regulatory methodology that differs meaningfully from the CMA's activities-based model. The ADGM approach is built around token-scoping: before any regulated activity can be conducted in relation to a virtual asset, the Authorised Person must determine whether that token qualifies as an Accepted Virtual Asset (AVA).

ADGM applies token-scoping criteria that include traceability, monitoring capability, security architecture, practical functionality, market liquidity, and the maturity of the underlying DLT ecosystem. These criteria are assessed on a risk-based basis for each individual token. A token that passes AVA assessment for one Authorised Person is not automatically accepted by another; each firm must conduct and document its own assessment.

The key AVA assessment criteria are:

- Traceability: Can on-chain transactions be traced to identifiable addresses or entities?

- Monitoring: Are adequate blockchain analytics tools available for the token's network?

- Security: Is the token's protocol architecture resistant to known attack vectors?

- Practical functionality: Does the token serve a genuine, defined purpose within its ecosystem?

- Market: Is there sufficient liquidity and price discovery for the token?

- DLT ecosystem: Is the underlying blockchain sufficiently mature and widely adopted?

ADGM's VA Regulated Activities rulebook links authorisation directly to Financial Services Permission (FSP) status, with the FSRA retaining discretion to impose additional risk mitigation measures on a case-by-case basis. This means that even after obtaining FSP authorisation, the FSRA may require enhanced controls for specific token types or business models.

"Compliance teams should treat token onboarding as a repeatable evidence pack, not a one-off exercise. Every new token requires fresh documentation, risk assessment, and sign-off against the AVA criteria."

This operational benchmark is particularly relevant for exchanges and custodians that regularly list or hold new assets. The ADGM framework does not permit a blanket approval of token categories; each asset requires individual assessment. For a detailed look at how ADGM virtual asset acceptance works in practice, including documentation standards, that resource covers the procedural requirements thoroughly.

The contrast between ADGM's token-first approach and the CMA's activity-first approach is significant. Under the CMA framework, you obtain authorisation for an activity and then operate within that permission. Under ADGM, you must also demonstrate that each asset you handle has been assessed and accepted before it can be included in your regulated activities. Both approaches are rigorous, but they require different compliance architectures.

Navigating activity mapping and multi-regulator overlap

Activity mapping is the process of systematically aligning your business's actual products and services to the regulatory categories defined by each applicable regulator. It sounds straightforward. In practice, it is where most licensing delays and compliance failures originate.

Mapping business activities and token mechanics to the regulator's categories is a gating step in the CMA framework. Get it wrong and your application will be returned, delayed, or refused. The CMA is explicit that client-asset custody requires separate prior endorsement, and ADGM requires documented risk methodology for every token. Neither regulator will accept vague or generic activity descriptions.

Common activity mapping mistakes include:

- Mis-classifying dealing as agent vs dealing as principal. These are distinct regulated activities with different capital and conduct requirements. If your platform executes trades on behalf of clients using client funds, that is dealing as agent. If you take positions on your own book, that is dealing as principal.

- Overlooking the custody endorsement requirement. Many applicants include custody in their activity list without realising that holding client assets requires a separate prior endorsement under the CMA framework.

- Failing to classify tokens correctly. Token classification drives regulatory pathways: a payment token triggers CBUAE oversight, an investment token triggers CMA/SCA jurisdiction, and a utility token may fall outside the regulated perimeter entirely. Misclassifying a token can result in operating without the correct authorisation.

- Assuming a single licence covers all activities. A VARA licence for exchange services does not cover investment advice or portfolio management. Each activity requires explicit authorisation.

For businesses operating virtual asset platforms in the UAE, the compliance obligations extend beyond licensing to ongoing systems, reporting, and conduct requirements. Similarly, virtual asset custody compliance involves a distinct set of operational and legal obligations that sit alongside the licensing endorsement.

Pro Tip: Build a regulatory mapping matrix at the outset of your licensing project. For each product or service, document the activity category, the applicable regulator, the token classification, and the evidence required. Treat this matrix as a live document that is updated whenever your product offering changes.

Practical steps for licensing and compliance in the UAE

A structured approach to UAE VASP licensing significantly reduces the risk of delays, rejections, and compliance gaps. The following sequence reflects the process that yields the most reliable outcomes for applicants across the CMA, VARA, and ADGM frameworks.

- Assess your business activities in granular detail. Document every product, service, and revenue stream. Do not describe activities at a high level; regulators require precise descriptions of how each function operates, who the counterparties are, and what assets are involved.

- Map each activity to the relevant regulatory category. Use the CMA's eight-activity framework, VARA's activity categories, or ADGM's FSP permissions as your reference. Identify which regulator has jurisdiction over each activity based on your operating zone and asset types.

- Classify every token or virtual asset you intend to handle. Determine whether each asset is a payment token, investment token, utility token, or other category. This classification determines which regulator applies and what additional requirements are triggered.

- Prepare your evidence pack for each activity and token. This includes governance documentation, AML/CFT policies, cybersecurity frameworks, capital adequacy evidence, and for ADGM applicants, AVA assessment documentation for each token.

- Identify whether a custody endorsement is required. If you will hold client assets at any point, initiate the CMA endorsement process as a parallel workstream, not an afterthought.

- Submit your application with complete, accurate documentation. Incomplete applications are a primary cause of delay. Regulators will return applications that lack required evidence or contain inconsistencies between the activity description and the supporting documentation.

ADGM Authorised Persons require documented, risk-based methodologies.pdf) for AVA assessments, and compliance teams should treat each token onboarding event as a repeatable evidence exercise. This principle applies equally to the CMA framework: compliance is not a one-time licensing event but an ongoing operational obligation.

For businesses operating as virtual asset brokers in the UAE, broker-specific conduct obligations add another layer to the compliance architecture. The AML compliance guide for UAE VASPs provides a detailed framework for meeting AML/CFT obligations under both federal law and regulator-specific requirements.

Pro Tip: Do not treat your AVA assessment or activity mapping documentation as a one-off submission. Build internal processes that trigger a fresh assessment whenever you add a new token, change a product feature, or expand into a new activity. Regulators expect ongoing compliance, not just initial approval.

Why activity mapping is the silent risk in UAE crypto regulation

In our experience advising VASPs across the UAE's regulatory landscape, the most consistent cause of licensing delays is not insufficient documentation or inadequate capital. It is premature assumptions about where a business fits within the regulatory framework.

Many founders and compliance teams approach licensing with a clear sense of what their business does, but a less precise understanding of how regulators categorise those activities. The gap between a business's self-description and the regulator's technical category definitions is where applications stall. A platform that describes itself as a "crypto exchange" may be conducting dealing as principal, dealing as agent, operating an MTF, and providing custody simultaneously. Each of those activities requires separate authorisation.

Token classification compounds this risk. A token that a business treats as a utility asset may be classified as an investment token by the regulator, triggering a completely different licensing pathway and a different set of obligations. The UAE's explicitly multi-regulator environment means that a misclassification at the outset can result in an application going to the wrong regulator entirely.

The lesson is that activity mapping and asset classification should be treated as dynamic, ongoing processes rather than one-off decisions made at the start of a licensing project. As your product evolves, your regulatory position evolves with it.

"Application success is less about ticking compliance boxes and more about the accuracy of your business-activity and asset mapping."

For businesses seeking financial consultancy compliance in the UAE, this principle is particularly relevant: the advisory and consultancy categories carry their own specific regulatory triggers that are frequently misidentified.

Expert support for UAE crypto licensing and compliance

Navigating the UAE's multi-regulator virtual asset landscape requires more than familiarity with the rules. It requires precise activity mapping, evidence-based token assessments, and a compliance architecture that holds up to regulator scrutiny across VARA, SCA/CMA, ADGM, and CBUAE.

CRYPTOVERSE Legal Consultancy provides specialist legal and compliance support for crypto startups and established VASPs at every stage of the licensing process. From pre-application activity mapping to full licence approval, we build regulator-ready evidence packs, design governance frameworks, and advise on AML/CFT policy aligned with FATF standards and UAE Federal AML Law. Whether you are pursuing VARA licensing in Dubai, SCA virtual asset licensing on the mainland, or authorisation within ADGM, our digital asset consultancy services deliver the legal precision your application requires.

Frequently asked questions

Which UAE regulator is responsible for crypto activities outside financial free zones?

The Securities and Commodities Authority (SCA) is the primary federal regulator for virtual assets outside financial free zones in the UAE, with the CBUAE covering payment token services.

What are the eight regulated virtual asset activities under the CMA framework?

The CMA's activities-based model covers dealing as principal, dealing as agent, providing custody, arranging custody, operating a multilateral trading facility, providing investment advice, portfolio management, and arranging investment deals.

How does ADGM determine which tokens are accepted virtual assets?

ADGM requires each Authorised Person to conduct a risk-based AVA assessment for every token, evaluating traceability, security, market liquidity, and DLT ecosystem maturity before recognising it as an Accepted Virtual Asset.

Is holding client assets under UAE regulation a separate licensing endorsement?

Yes. The CMA framework requires a distinct prior endorsement for holding client assets, with additional obligations around segregation and client money protection that sit alongside the standard custody activity authorisation.

What is the main pitfall for UAE VASPs seeking licensing?

Failure to accurately map business activities and token mechanics to regulatory categories is the most common licensing pitfall, often resulting in applications being submitted to the wrong regulator or returned for insufficient evidence.