TL;DR:

- Operating across multiple crypto markets without a structured compliance framework exposes firms to legal risks, licensing gaps, and enforcement actions. A comprehensive multi-jurisdiction regulation guide helps virtual asset service providers ensure proper classification, licensing, AML/CFT compliance, and governance standards aligned with 2026 developments in the US, UK, EU, and UAE. Effective governance, timely registration, and ongoing classification management are essential to resilient international crypto operations.

Operating across multiple crypto markets without a structured compliance framework is not merely inconvenient. It creates material legal exposure, licensing gaps, and enforcement risk that boards and general counsel cannot afford to ignore. This multi-jurisdiction crypto regulation guide addresses the regulatory complexity that virtual asset service providers (VASPs), token issuers, and digital asset funds face when expanding internationally. Covering classification mandates, licensing timelines, AML/CFT obligations, governance standards, and strategic structuring, this guide draws on the most consequential 2026 regulatory developments across the US, UK, EU, and UAE.

Multi-jurisdiction crypto regulation: core classifications

How a jurisdiction classifies a crypto asset determines every compliance obligation that follows. Classification is the threshold question, and getting it wrong at the outset compounds every subsequent decision about registration, product design, and marketing.

The US SEC-CFTC unified framework

In March 2026, the SEC and CFTC clarified how federal securities laws apply to crypto assets, issuing joint guidance on token taxonomy, the treatment of airdrops, staking, and wrapping, and the conditions under which a non-security crypto asset can become an investment contract. The practical effect is that classification is not a one-time legal opinion. It is an ongoing compliance control that responds to how a token is marketed, distributed, and governed over time.

The SEC-CFTC joint interpretative release makes clear that contemporaneous evidence of marketing narratives and governance controls forms part of the evidentiary record a regulator will examine.

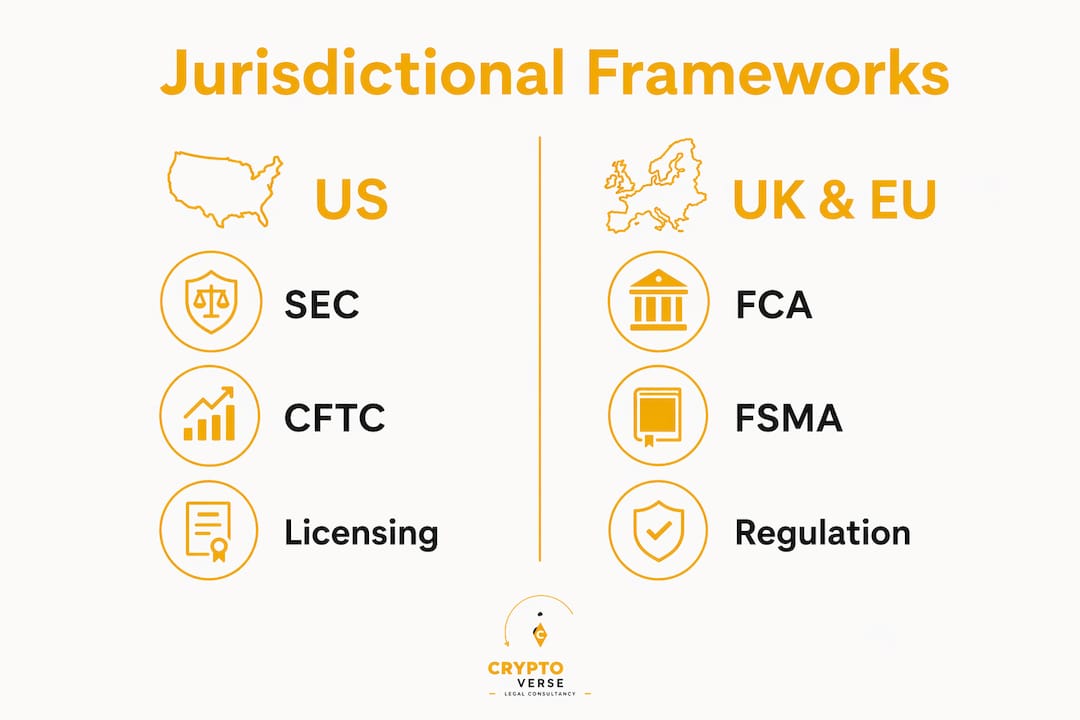

UK and EU classification frameworks

In the UK, the Financial Conduct Authority's FSMA cryptoasset regime treats cryptoassets as a designated investment activity. Separately, firms must maintain registration under the Money Laundering Regulations (MLRs) until the FSMA regime is fully operational. The EU's Markets in Crypto-Assets regulation (MiCA) introduces a three-tier asset classification: asset-referenced tokens, e-money tokens, and other crypto-assets, each carrying distinct authorisation requirements and capital obligations.

Pro Tip: Classification under one framework does not guarantee equivalence in another. A utility token that falls outside MiCA's e-money token category may still attract securities law treatment in the United States if its marketing emphasises profit expectations.

The table below summarises classification differences and core compliance mandates across the three major markets.

| Jurisdiction | Primary classification framework | Regulator | Key compliance trigger |

|---|---|---|---|

| United States | Securities Act / Howey Test + 2026 SEC-CFTC guidance | SEC, CFTC | Investment contract analysis; marketing evidence |

| United Kingdom | FSMA 2000 (amended); MLR registration | FCA | MLR registration; FSMA authorisation from Oct 2027 |

| European Union | MiCA Regulation | ESMA, NCAs | Asset-referenced token; e-money token; other crypto |

| UAE | VARA Virtual Assets Regulation; SCA Decision No. 23/2020 | VARA, SCA, DFSA, FSRA | VASP licence; activity-specific approval |

Licensing, registration, and authorisation pathways

Understanding classification is a prerequisite. Acting on it through timely registration and authorisation is where most firms encounter operational difficulty, particularly when managing concurrent applications across several jurisdictions.

UK FCA registration and FSMA authorisation

The FCA operates two separate but concurrent processes. Firms must register under the MLRs before the new FSMA regime commences. The FSMA application gateway opens on 30 September 2026, with the regime effective 25 October 2027. The MLR registration deadline is 31 July 2027, and applications submitted after this date are unlikely to be decided in time, with a standard assessment timeframe of three months applying.

Firms that treat these as sequential processes rather than concurrent ones risk gaps in regulatory coverage. The FCA processes both applications separately. Planning submissions to account for processing timelines is therefore a precondition for uninterrupted operations.

UAE licensing under VARA and SCA

The UAE offers one of the most structured multi-regulator environments for VASPs. VARA governs virtual asset activities in Dubai (outside DIFC), while the SCA regulates exchanges and certain token offerings at the federal level. The DFSA's rulebooks, including COBS, AML, and GEN, apply within the DIFC. The FSRA administers a separate virtual asset framework within the Abu Dhabi Global Market. Depending on the activity and geography, a firm may need to engage multiple regulators simultaneously.

For detailed guidance on VARA licensing and the applicable VARA compliance requirements, firms should assess their activity categories against VARA's Rulebooks before submitting a pre-application.

Recommended preparatory actions

Firms approaching multi-jurisdiction licensing should address the following before submitting any application:

- Map each licensable activity by jurisdiction and identify the primary regulator for each.

- Conduct a classification analysis under US, UK, EU, and UAE frameworks before finalising token design or product architecture.

- Appoint a compliance officer and board-level sponsor with defined accountability for regulatory submissions.

- Draft AML/CFT policies aligned with FATF standards and, where applicable, UAE Federal AML Law (Decree-Law No. 20 of 2018 and its amendments).

- Prepare governance documentation covering client asset segregation, capital adequacy, and operational resilience.

- Engage external legal counsel in each target jurisdiction at least six months ahead of intended market entry.

Pro Tip: For UK-bound operations, treat MLR registration and FSMA authorisation as simultaneous workstreams. Firms that sequence them risk a gap in regulatory status that can interrupt business continuity and trigger client notification obligations.

AML/CFT obligations and the FATF Travel Rule

AML/CFT compliance is the area where international crypto regulations converge most directly on operational systems. The FATF Travel Rule, derived from Recommendation 16, requires VASPs to collect, hold, and transmit originator and beneficiary information for virtual asset transfers above defined thresholds.

| Jurisdiction | Travel Rule threshold | Competent authority | Implementation instrument |

|---|---|---|---|

| United States | USD 3,000 (existing BSA rule) | FinCEN | Bank Secrecy Act; proposed NPRM extensions |

| United Kingdom | GBP 1,000 | FCA | MLR 2017 (amended); JMLSG guidance |

| European Union | EUR 0 (no de minimis under TFR) | ESMA, NCAs | Transfer of Funds Regulation (TFR) |

| UAE | AED 3,500 (approx. USD 1,000) | VARA, CBUAE | CBUAE Circular 2/2024; VARA AML Rulebook |

| Switzerland | CHF 1,000 | FINMA | AMLA; FINMA Guidance 02/2019 |

The FATF baseline sets thresholds at around USD/EUR 1,000, but the EU's Transfer of Funds Regulation removes the de minimis entirely, requiring full originator and beneficiary data for all transfers regardless of value.

Operational compliance requires firms to implement VASP-to-VASP data exchange, verify counterparty VASP registration status, and apply risk-based controls when transacting with unhosted wallets. For cross-border transactions, the strictest applicable Travel Rule standard should govern data collection as a default, since a firm cannot know at point of initiation which jurisdiction's rules will apply to the receiving entity.

Technology solutions facilitating compliant Travel Rule transmission, including interoperable networks for private, secure data exchange between VASPs, are becoming a baseline expectation for regulated firms rather than an optional enhancement.

Governance, technology controls, and risk management

Regulators across all major jurisdictions are raising their expectations of governance structures within crypto firms, particularly as the sector attracts institutional participation and retail investor exposure increases.

Board-level governance and prudential standards

The UK FSMA crypto regime and UAE VARA regulations both emphasise board-level supervision, capital adequacy, client asset segregation, and operational resilience as non-negotiable conditions for authorisation. Boards must be able to demonstrate active oversight of compliance risk, not merely delegation to a compliance officer.

Capital adequacy requirements vary by activity. Custody providers face different prudential thresholds than exchange operators or token issuers. Firms with multi-jurisdiction operations should model capital requirements against the most demanding applicable standard.

Recommended technology and operational controls

- Implement a custody model that segregates client assets from firm assets at the wallet level, with independent reconciliation.

- Deploy transaction monitoring systems capable of screening against OFAC, UN, EU, and UAE sanctions lists simultaneously.

- Maintain a market abuse and manipulation detection framework applicable to any trading venue activity.

- Establish documented operational resilience procedures including recovery time objectives and incident response protocols aligned with VARA's Technology Governance Rulebook and FCA operational resilience guidance.

- Use blockchain analytics tools to support Travel Rule counterparty verification and unhosted wallet risk assessment.

- Preserve contemporaneous records of all marketing materials, token distribution decisions, and governance changes as part of the evidentiary control framework required under the SEC-CFTC 2026 guidance.

Strategic structuring for multi-jurisdictional operations

Designing the optimal regulatory architecture for an international crypto business requires weighing licensing complexity, capital obligations, operational costs, and time-to-market across competing jurisdictions.

Regulatory hub comparison

| Jurisdiction | Licensing complexity | Time to licence | Capital requirements | Key advantage |

|---|---|---|---|---|

| UAE (VARA) | Moderate | 6–12 months | Activity-dependent | Crypto-native regulator; 5 regulators covering all activities |

| UK (FCA) | High | 12–18 months | FCA-specified | Access to EU and global counterparts; FSMA regime certainty |

| EU (MiCA) | Moderate to high | 6–18 months | Tiered by asset class | EU passporting rights across 27 member states |

| United States | Very high | 18–36 months | State and federal levels | Largest retail and institutional market globally |

| Switzerland | Moderate | 6–12 months | FINMA-specified | Stable legal framework; VASP-friendly banking access |

The UAE stands out for offering a crypto-specific regulatory framework under VARA with clearly defined VASP categories, activity-specific approval pathways, and a regulator that engages proactively with applicants. For firms requiring EU market access, the EU crypto-asset framework under MiCA provides passporting rights that justify the additional authorisation burden.

Token classification risk management requires ongoing documentation. Firms should preserve marketing evidence and governance records from the point of token design through to post-launch distribution, as these form the evidentiary basis for any classification defence. The SEC-CFTC joint guidance makes this a formal compliance expectation, not merely prudent legal hygiene.

For firms considering Swiss incorporation as part of a multi-entity structure, the Swiss crypto incorporation framework offers a structurally sound option with established FINMA oversight and access to crypto-friendly banking.

Our perspective on multi-jurisdiction compliance

In my experience advising VASPs, exchanges, and token issuers across the UAE and internationally, the most persistent error I see is treating classification as a completed task rather than an active compliance control. A legal opinion obtained at the point of token design becomes unreliable the moment the marketing team adjusts its messaging or the product team introduces a staking mechanism. The 2026 SEC-CFTC guidance has formalised what careful practitioners have known for years: the evidentiary record you build around product decisions is as important as the legal analysis itself.

I have also seen firms systematically underestimate FCA registration timelines. The three-month assessment window is a minimum, not a guarantee, and firms that delay engagement because they consider the FSMA gateway a more important milestone frequently find themselves without regulatory status when the regime becomes operative.

What I believe distinguishes well-structured international crypto businesses is not their legal opinions. It is their governance architecture. Firms that integrate legal, product, and compliance teams into a single review cycle before go-to-market, and that maintain evidentiary control over every material decision, are the ones that withstand regulatory scrutiny without material disruption.

The technology layer is catching up. Interoperable Travel Rule networks are reducing one of the most operationally complex compliance burdens. But technology does not substitute for governance. The board must own the compliance framework, not merely sign off on it.

— CRYPTOVERSE

How Cryptoverselawyers supports your compliance strategy

Cryptoverselawyers is a Dubai-based legal consultancy specialising exclusively in virtual assets, blockchain, and fintech regulation. We advise across all five UAE crypto regulators, including VARA licensing and SCA authorisation, and extend structured legal support to over 30 jurisdictions worldwide.

Our services cover the full compliance lifecycle: VASP licence applications from pre-submission to approval, AML/CFT policy design aligned with FATF standards and UAE Federal AML Law, token classification and marketing review, governance framework design, and multi-entity corporate structuring. If your firm is preparing for FCA registration, MiCA authorisation, or a VARA application, our team can provide a digital asset compliance audit and tailored legal roadmap. Contact Cryptoverselawyers to discuss your regulatory exposure and structuring options.

FAQ

What is a multi-jurisdiction crypto regulation guide?

A multi-jurisdiction crypto regulation guide is a structured legal and compliance reference that maps regulatory requirements, classification rules, licensing obligations, and AML/CFT standards across multiple countries simultaneously, enabling businesses to manage cross-border regulatory risk systematically.

Which jurisdictions have the most demanding crypto licensing requirements?

The United States has the most complex framework, requiring state-level money transmission licences alongside potential federal registration, with timelines of 18 to 36 months. The UK FCA and EU MiCA regimes are also demanding, though MiCA offers passporting rights across EU member states as a commercial offset.

When must UK crypto firms register under the FCA's new FSMA regime?

The FSMA application gateway opens 30 September 2026, with the regime effective 25 October 2027. Firms must register under the MLRs by 31 July 2027 to maintain continuity of regulatory status, as applications submitted after this date are unlikely to be processed in time.

What does the FATF Travel Rule require from crypto businesses?

The Travel Rule requires VASPs to collect and transmit originator and beneficiary information for virtual asset transfers above jurisdictional thresholds. The EU applies a zero threshold under its Transfer of Funds Regulation, while the UAE, UK, and Switzerland apply thresholds of approximately USD/EUR 1,000.

How does UAE crypto regulation differ from EU and UK frameworks?

The UAE operates five separate crypto regulators, with VARA governing most virtual asset activities in Dubai. Unlike the EU's single MiCA framework or the UK's FCA-led FSMA regime, the UAE requires firms to identify the correct regulator by activity type and geographic location, which can result in concurrent authorisation obligations under VARA, SCA, or DFSA depending on the business model.