TL;DR:

- UAE's crypto compliance framework now requires precise activity-level licensing, capital, and product alignment.

- Dubai's VARA introduces a detailed derivatives rulebook with strict retail leverage limits and active risk controls.

- Global regimes differ significantly, with strict conduct rules in EU, stablecoin focus in US, and flexible but demanding requirements in UAE.

Many executives at virtual asset service providers still operate under the assumption that the UAE's crypto compliance environment is relatively uniform and that a single licence grants broad operational latitude. That assumption is increasingly costly. The UAE's federal and emirate-level regulators are now issuing distinct, detailed frameworks with tiered capital requirements, prohibited token categories, and updated rulebooks for derivatives. Simultaneously, the UK, EU, and US are tightening their own regimes. This guide breaks down the critical rules, benchmarks, and practical steps your VASP needs to meet today's compliance standards and position for sustainable growth.

Key Takeaways

| Point | Details |

|---|---|

| UAE compliance scope | The UAE’s new federal regime defines eight distinct licensed VASP activities and sets capital benchmarks. |

| Dubai derivatives rules | VARA’s latest rulebook brings strict caps on leverage and grants regulators swift enforcement powers. |

| International contrasts | UK, EU, and US frameworks differ on stablecoins, fines, and VASP application windows. |

| Edge-case risks | Reverse solicitation, prohibited tokens, and evolving regulatory demands pose hidden operational pitfalls. |

| Proactive compliance strategy | Mastering scenario planning and regulatory empathy is key for VASPs aiming for lasting compliance success. |

Understanding the new UAE federal crypto compliance framework

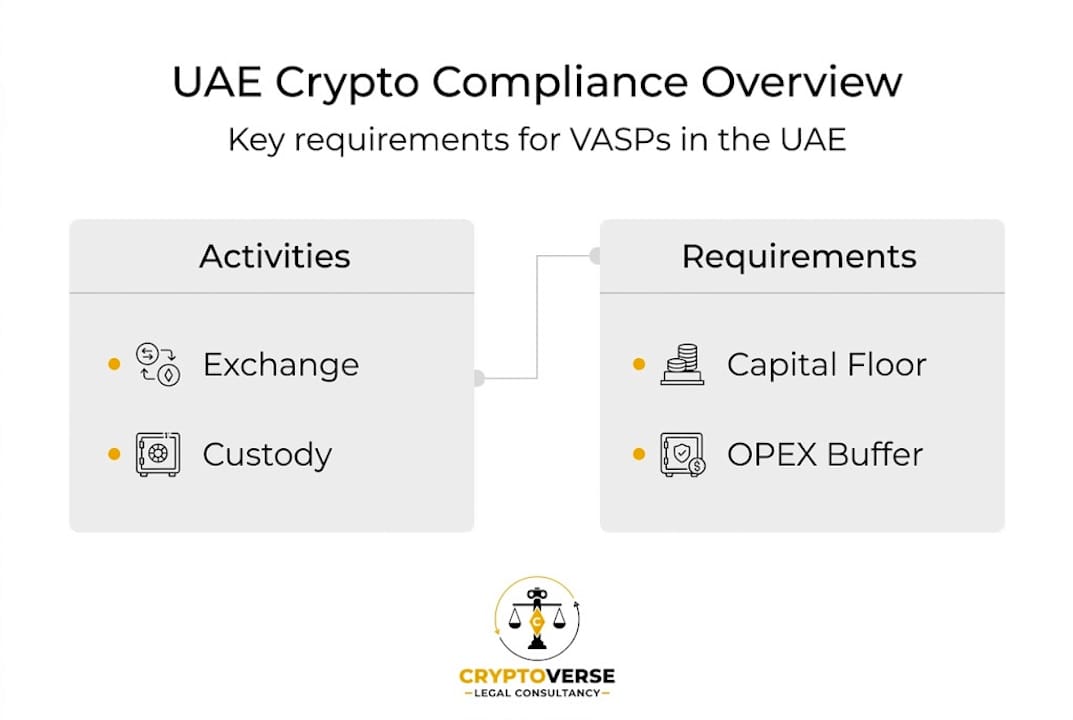

The UAE's federal regulatory architecture for virtual assets has shifted materially in 2026. UAE CMA Decision No. 4/R.M/2026 establishes a federal framework for VASPs covering eight distinct licensed activities. This is not an incremental update. It represents a structured, risk-stratified approach that requires every VASP operating under the SCA's federal remit to align its corporate structure, capital base, and operational controls with specific activity-level obligations.

The eight licensed activities under CMA Decision No. 4/R.M/2026 are:

- Exchange services (spot and conversions)

- Custody services (safeguarding client assets)

- Broker-dealer services (facilitating trades on behalf of clients)

- Advisory services (providing investment guidance on virtual assets)

- Portfolio management (discretionary and non-discretionary management)

- Lending and borrowing (including margin and collateralised lending)

- Transfer and settlement services (processing VASP-to-VASP and client transfers)

- Management and investment (fund-level and collective scheme activity)

Each activity carries its own capital floor. Capital requirements are tiered by risk, ranging from AED 500,000 for advisory services up to AED 4 million or more for exchange and custody activities, plus a mandatory six-month operational expense buffer. The table below summarises this structure:

| Licensed activity | Minimum capital (AED) | OPEX buffer required |

|---|---|---|

| Advisory | 500,000 | 6 months |

| Portfolio management | 1,000,000 | 6 months |

| Broker-dealer | 2,000,000 | 6 months |

| Transfer and settlement | 2,000,000 | 6 months |

| Lending and borrowing | 3,000,000 | 6 months |

| Exchange | 4,000,000+ | 6 months |

| Custody | 4,000,000+ | 6 months |

| Management and investment | Variable | 6 months |

Beyond capital thresholds, the framework introduces strict prohibitions on certain token categories. Privacy tokens such as Monero and algorithmic stablecoins are prohibited under this federal framework. Fiat-backed stablecoins, by contrast, are permitted but subject to a 1:1 reserve requirement backed by verifiable, high-quality liquid assets, with monthly independent audits. This distinction matters enormously for platforms planning multi-product offerings.

For safe custody compliance in the UAE, VASPs must maintain segregated client asset accounts, implement cold storage policies for a defined proportion of holdings, and demonstrate operational resilience through documented business continuity plans.

Pro Tip: When calculating your six-month OPEX buffer, include projected regulatory filing fees, audit costs, and technology maintenance expenditure. VASPs frequently underestimate these line items during the pre-application phase, which leads to capital shortfall findings during FSRA or SCA review.

Taken together, this framework signals that UAE compliance for VASPs is no longer a matter of meeting a general fitness-and-propriety standard. It demands precise structural alignment between your licensed activities, your capitalisation, and your product catalogue.

Dubai VARA's derivatives rulebook and risk controls

With the federal picture clear, we move to Dubai's pivotal rulebook shaping derivatives and risk management. The Virtual Assets Regulatory Authority's updated framework, commonly referred to as VARA Rulebook v2.1, introduces a dedicated exchange-traded derivatives framework for virtual assets. This is a landmark development. Until recently, crypto derivatives in Dubai operated in a regulatory grey zone, with VASPs often relying on general activity permissions that did not specifically address futures, perpetuals, options, or contracts for differences.

VARA's ETD framework now explicitly covers crypto futures, perpetual swaps, options, and CFDs. Retail investors face a leverage cap of 5:1, with a 20% initial margin requirement. Professional and institutional clients are subject to separate thresholds, but VASPs must implement robust client classification processes to correctly apply the relevant limits.

The following comparison illustrates how VARA's retail limits sit against international benchmarks:

| Jurisdiction | Retail leverage cap | Initial margin | Regulatory authority |

|---|---|---|---|

| Dubai (VARA) | 5:1 | 20% | VARA |

| UK (FCA) | 2:1 | 50% | FCA |

| EU (ESMA guidance) | 2:1 | 50% | National NCAs |

| Singapore (MAS) | 2:1 | 50% | MAS |

This positions Dubai's crypto regulation as comparatively more permissive on leverage than Western jurisdictions while still imposing credible safeguards. For VASPs targeting professional client flows, this creates a meaningful competitive advantage.

Steps VASPs should follow for suitability reassessments under VARA's updated rulebook:

- Conduct a full product inventory review to identify all existing derivative offerings and map them against the ETD framework definitions.

- Reclassify all active clients using VARA's updated retail and professional investor criteria, including net worth thresholds and trading experience requirements.

- Amend client agreements and risk disclosure documents to reflect new leverage limits and margin call procedures.

- Update your trade surveillance systems to flag positions exceeding retail leverage thresholds in real time.

- Submit a written compliance attestation to VARA confirming that all required systems and controls are operational before resuming or launching derivative products.

One critical feature of the updated framework often overlooked in internal compliance reviews: VARA retains the power to order immediate remedial actions against a VASP without advance notice. This means your incident response procedures must be pre-drafted and tested, not assembled reactively.

"VARA can order immediate actions without notice under the updated derivatives framework. VASPs that lack pre-approved escalation protocols and board-level response authorities will face compounded regulatory risk at the moment they can least afford it."

Pro Tip: Establish a standing internal VARA response committee with pre-authorised decision-making authority. Map out at least four immediate-action scenarios — including temporary trading halts, client notifications, and asset freezes — so that your response is measured and documented from the first hour. For virtual asset transfer and exchange rules under VARA, documented protocols are equally essential.

Review the full scope of VARA updated crypto rules to ensure your derivatives compliance programme addresses every applicable obligation.

International benchmarks: UK FCA, EU, and US stablecoin rules

Having outlined UAE specifics and Dubai's rulebook, it is crucial to compare global compliance benchmarks affecting VASPs in multinational contexts. The UK, EU, and US are each implementing distinct frameworks in 2026, and for VASPs operating or planning to operate across multiple jurisdictions, misaligned compliance programmes are an immediate risk.

UK FCA crypto regime

The UK FCA authorisation window runs from September 2026 to February 2027 for firms seeking full authorisation under the new cryptoasset regulations. Stablecoins are now explicitly brought within the UK payments perimeter, meaning any VASP facilitating stablecoin payments for UK-connected clients must hold or apply for the appropriate payment institution authorisation alongside its crypto-specific licence. Crypto dealing activity remains within the regulated perimeter until at least 2027, providing a brief transition window but no exemption from existing registration requirements.

Key UK compliance priorities for VASPs include:

- Reviewing whether current FCA registration status is sufficient or whether full authorisation is now required

- Assessing whether stablecoin activities bring the firm within the payments perimeter

- Updating AML/CFT policies to satisfy FCA's enhanced cryptoasset-specific expectations

- Confirming travel rule implementation meets the UK's current technical standards

EU MiCA framework

The EU MiCA framework is now fully in force, with substantial fines available to national competent authorities for breaches of authorisation and conduct obligations. MiCA imposes capital requirements broadly comparable to the lower tiers of the UAE's CMA Decision, but its conduct-of-business rules, particularly around marketing communications and asset-referenced token issuance, are significantly more prescriptive.

US GENIUS Act and stablecoin regulation

In the United States, stablecoin issuers under the GENIUS Act must implement AML/CFT programmes meeting Bank Secrecy Act standards. Notably, the GENIUS Act does not require secondary market monitoring by issuers, which limits certain compliance obligations but places pressure on exchange-layer VASPs. Treasury rulemaking was proposed in April 2026, establishing the timeline for formal regulatory implementation. Utility tokens continue to sit in an ambiguous classification zone under US federal law, which creates planning uncertainty for issuers with cross-border distribution.

The table below sets out a consolidated view of application timelines and key obligations across jurisdictions:

| Jurisdiction | Application window | Stablecoin treatment | Fines available |

|---|---|---|---|

| UAE (federal) | Open | 1:1 reserves, monthly audit | Yes |

| Dubai (VARA) | Open | Activity-specific | Yes |

| UK (FCA) | Sept 2026 to Feb 2027 | Payments perimeter | Yes |

| EU (MiCA) | Ongoing | ART/EMT rules | Significant |

| US (GENIUS Act) | TBC (Treasury rules) | AML programme required | Yes |

For a practical comparison of crypto law benchmarks across jurisdictions, reviewing regional licensing frameworks side by side is an effective starting point for multinational strategy planning.

Edge cases and practical pitfalls: Prohibited tokens, reverse solicitation, and VASP readiness

To build on international benchmarking, let's tackle the specific pitfalls VASPs must avoid, including hidden traps in token offering, solicitation, and rapid reassessment.

Prohibited token categories

UAE federal law prohibits privacy tokens and algorithmic stablecoins, and VARA's ongoing suitability reassessments include a review of listed instruments on exchange platforms. If your platform currently lists any token with obfuscation features, anonymous transaction capabilities, or algorithmic supply-adjustment mechanisms, those assets must be delisted before or at the point of licence application. Failure to do so is not merely a technical breach. It signals poor compliance culture and materially weakens your application.

Additional prohibited and restricted categories to review include:

- Tokens linked to sanctioned jurisdictions or individuals (OFAC, UN, UAE sanctions lists)

- Tokens constituting unregistered securities in any applicable jurisdiction where clients are served

- Tokens issued by entities on VARA or SCA watchlists

- Stablecoins without verifiable reserve audits or issued by entities without regulatory authorisation

Reverse solicitation under EU MiCA

Reverse solicitation, where a client initiates contact with a third-country VASP without any prior marketing, is a narrow exemption under MiCA and is frequently misapplied. Adding a disclaimer to a website or terms and conditions document does not convert active marketing into reverse solicitation. The MiCA reverse solicitation exemption is narrow, and regulators will examine the substance of client acquisition, not just documentation. If your marketing, CRM, or partner referral activity touches EU-resident clients, you are almost certainly outside the exemption.

"The contrast across global regimes is instructive: the UAE combines innovation latitude with integrity controls; the EU prioritises investor safety through prescriptive conduct rules; the US is stablecoin-focused while utility token classification remains unresolved. Each regime reflects distinct policy priorities, and VASPs must plan product strategies accordingly."

Operational agility under evolving rules

For broker VASP compliance, maintaining operational agility means building compliance review cycles into your quarterly governance calendar, not treating them as ad hoc exercises. The 2026 UAE virtual asset AML guide reinforces that AML/CFT programme reviews must be continuous and documented.

Pro Tip: Establish a regulatory change log maintained by your compliance function. Each time VARA, SCA, or an international regulator issues updated guidance, log the change, assign an impact rating, and document the internal response. This log becomes invaluable evidence of proactive compliance culture during supervisory inspections.

Our perspective: Compliance mastery is more than ticking boxes

Across the VASPs we work with, the ones that fare best in regulatory reviews are not necessarily those with the largest compliance teams or the most expensive technology systems. They are the ones that have internalised a risk anticipation mindset at the executive level. Compliance is treated as a strategic input, not an administrative output.

The recent regulatory shifts across the UAE, UK, EU, and US share one common feature: they reward structured preparation and penalise reactive adjustment. VASPs that mapped their product catalogue against CMA Decision No. 4/R.M/2026 six months before enforcement had time to delist, recapitalise, and update governance documents without operational disruption. Those that waited scrambled.

Regulatory empathy, meaning a genuine effort to understand what a regulator is trying to achieve with a given rule, produces better compliance design than mechanical rule-reading. Web3 compliance trends in 2026 consistently point to the same conclusion: the firms building durable compliance frameworks are those whose legal, product, and executive teams talk to each other regularly and align on risk tolerance before problems emerge.

Expert legal support for crypto licensing and compliance

Navigating the layered demands of CMA Decision No. 4/R.M/2026, VARA's updated derivatives rulebook, and international frameworks such as MiCA and the GENIUS Act requires more than general legal advice. It requires specialists who understand both the regulatory text and the operational realities of running a virtual asset business.

CRYPTOVERSE Legal Consultancy advises VASPs across every UAE regulator, from VARA licensing and compliance through to SCA licensing applications and federal framework structuring. Our team covers the full licence lifecycle, including AML/CFT programme design, capital structuring, token classification reviews, and supervisory correspondence. Whether you are applying for the first time or realigning an existing licence to meet updated requirements, our digital asset legal services are built for the complexity you face.

Frequently asked questions

What activities require a UAE crypto licence under CMA Decision No. 4/R.M/2026?

Eight activities are licensed under this framework: exchange, custody, broker-dealer, advisory, portfolio management, lending and borrowing, transfer and settlement, and management and investment. Each activity carries its own capital requirement and compliance obligations.

What are the new retail leverage limits for crypto derivatives in Dubai?

Retail investors face a 5:1 leverage cap under VARA's updated derivatives framework, with a 20% initial margin requirement on exchange-traded derivative products including futures, perpetuals, options, and CFDs.

How does the UK FCA crypto regime affect stablecoin payments?

Stablecoins are now within the UK payments perimeter, meaning VASPs facilitating stablecoin transactions for UK clients must hold appropriate authorisation. The application window runs from September 2026 to February 2027.

Are privacy tokens allowed in the UAE?

No. Privacy tokens such as Monero and algorithmic stablecoins are federally prohibited under CMA Decision No. 4/R.M/2026, and VASPs must delist or refrain from listing these asset types to maintain regulatory standing.

What are common pitfalls when applying for a crypto licence in the UAE?

Regulatory edge cases, rapid rule changes, and operational expense buffer miscalculations are frequent causes for application rejection or significant delay. Firms that underestimate the scope of prohibited token reviews and suitability reassessments routinely encounter material setbacks at advanced stages of the approval process.